A few years ago, I used to think wealth building was something only financially smart or rich people could do. But by 2025, I realized that smart money moves actually start with simple things—small steps that anyone can take. The journey wasn’t easy for me either. I was also the person who would open the shopping cart as soon as the salary arrived. But when I started tracking my spending, improved my financial habits, and adopted long-term thinking—that’s when my finances slowly began to change.

Today, I can say from my experience that wealth building is not tough; it just requires discipline and clarity.

1. Tracking Spending: The Simplest and Most Powerful Step

My biggest problem was that I didn’t even know where my money went. I thought I didn’t spend much—but when I used a simple free expense tracker app last year, I was shocked. In just one week, I found out about:

- 4 times coffee

- 2 times random food delivery

- Unnecessary subscriptions

- Impulsive weekend shopping

The total? More than ₹6,000 wasted in a month. The first step to a smart money move in 2025 is this: Track your spending.

I would take 2 minutes every day to log my expenses. This helped me figure out which habits were financially draining me. Trust me, this step was a game-changer for me.

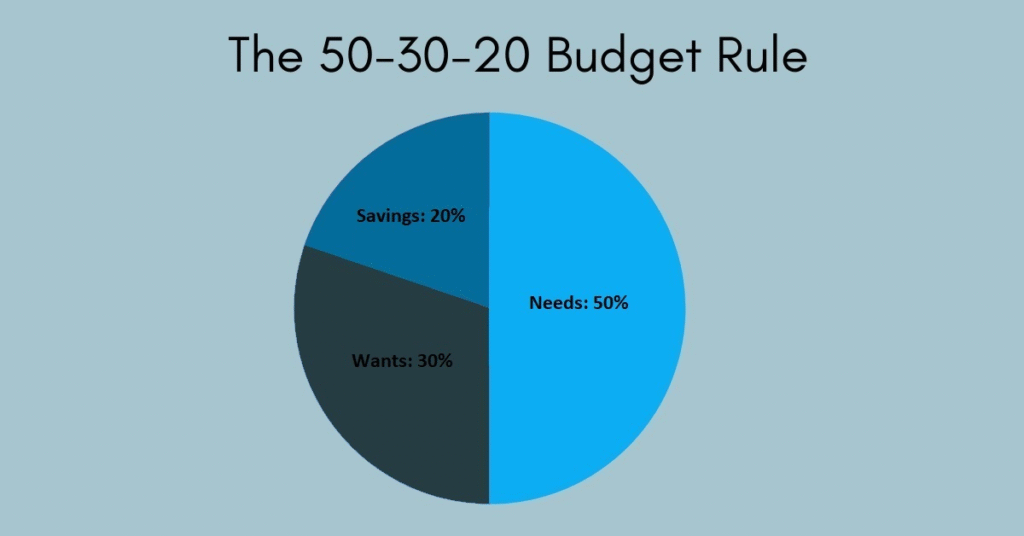

2. The 50-30-20 Rule: The Budget That Finally Worked

Before, I would try to budget, but after a day or two, I would forget.

But the 50-30-20 rule simplified my life:

- 50% – Needs: Rent, groceries, bills

- 30% – Wants: Dining out, entertainment

- 20% – Savings/Investments

This gave me clarity on how much I should save every month without burdening my lifestyle. In the time of inflation in 2025, this rule is still practical; it just requires a little adjustment.

Sometimes, my ‘Wants’ part goes from 30 to 20, and ‘Saving’ goes from 20 to 30—depending on my goals.

3. Creating an Emergency Fund: My Mental Peace Bank

In 2023, when an unexpected expense came up during my health checkup, I realized how important an emergency fund is. I only had ₹5,000 left then, and I had to borrow money from outside.

That’s when I decided that an emergency fund would now be compulsory.

My emergency fund goal for 2025 is: Keep 3–6 months of expenses in a separate account.

I started with just ₹500 per week. Slowly, it grew into a good amount.

Now I know that financial shocks can be handled without stress.

4. Starting Investment: Small Start, Big Difference

Earlier, I found investing risky. I thought the stock market was only for experts But when I started with an SIP—just ₹1,000 per month—I felt financially empowered.

My investment plan in 2024 was simple:

- Mutual Funds (SIP)

- Index Funds

- Digital Gold (very small portion)

In 2025, I am diversifying a bit:

- Blue-chip stocks (very carefully)

- More index funds

- High-interest savings account

My learning: Investing is not complicated; the mindset is complicated. When you take small steps, your confidence automatically grows.

5. Canceling Useless Subscriptions: Small Step, Big Savings

There was a time when I had 9+ subscriptions—apps, OTT platforms, music, even a gaming app that I didn’t use. When I listed all my subscriptions, I realized I was wasting ₹1,200 a month just on unused apps.

So I made a simple rule: If not used in 30 days — CANCEL.

This increased my annual savings by almost ₹12,000—without any effort.

6. Side Income: 2025’s Most Underrated Smart Money Move

I always thought that side income could only be generated by freelancers or influencers. But then I realized that anyone can create a side income. I personally tried this:

- Weekend online tasks

- Small content writing gigs

- Selling unused items

- Tutoring part-time

Even an extra ₹4,000–₹5,000 per month fast-tracked my savings goals. In 2025, creating a side income I think has become not optional but necessary—even if it’s small.

7. Using Credit Card Smartly

Earlier, I used to treat my credit card as “free money” (yes, a mistake!). There was overspending, followed by guilt after seeing the bill.

In 2025, I only follow these rules:

- Full payment before the due date.

- Only use cashback cards.

- Only planned purchases.

This gives me reward points and also improves my credit score.

8. Creating Clear Financial Goals: The Roadmap That Worked for Me

Before, my goals were vague—”I need to save money.” But vague goals don’t provide motivation. Now my financial goals are clear, written, and achievable:

- ₹1 lakh emergency fund in 2025.

- ₹25k mutual fund investment by March.

- Vacation budget of ₹20k without loans.

- Increase income savings by 10% by year-end.

Clarity is power. When the target is clear, the action automatically gets sorted out.

Conclusion: Wealth Building Is a Journey, Not a Race

The meaning of wealth building changed for me in 2025. It’s not about earning more—it’s about managing better.If you are a beginner, just start with these 3 steps:

- Track your spending.

- Create a budget.

- Start an SIP (even with ₹500).

Small steps make the biggest difference.The smart money moves that seem small today will become the foundation of your financial stability in the future.

Note: This blog is based purely on my personal experiences and understanding of money management. I am not a certified financial advisor. The strategies and suggestions shared here may not work the same way for everyone. Before making any financial decisions, please consider your personal situation or consult a professional financial expert. All information is for educational and motivational purposes only.

#SmartMoney2025#WealthBuildingTips#PersonalFinanceJourney#MoneyManagement2025#FinancialFreedomGoals#BudgetingMadeEasy #InvestingForBeginners#SavingsStrategies#FinanceBlog2025#WealthMindset#Carrerbook#Anslation